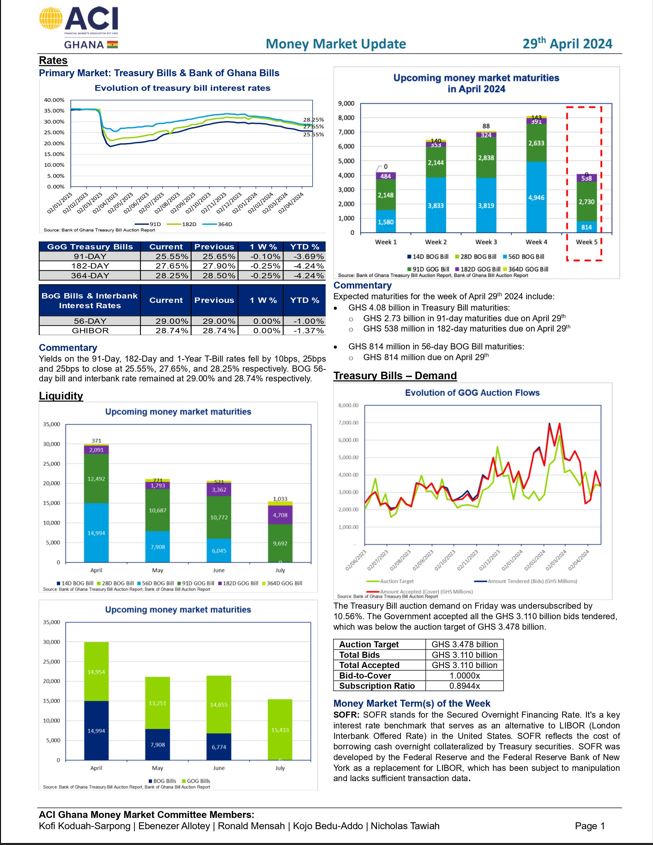

Yields on the 91-Day, 182-Day and 1-Year T-Bill rates fell by 10bps, 25bps and 25bps to close at 25.55%, 27.65%, and 28.25% respectively. BOG 56- day bill and interbank rate remained at 29.00% and 28.74% respectively.

Expected maturities for the week of April 29, 2024, include:

>> GHS 4.08 billion in Treasury Bill maturities comprising:

- GHS 2.73 billion in 91-day maturities due on April 29th

- GHS 538 million in 182-day maturities due on April 29th

>> GHS 814 million in 56-day Bill maturities comprising:

- GHS 814 million due on April 29th

The Treasury Bill auction demand on Friday was undersubscribed by 10.56%. The Government accepted all the GHS 3.110 billion bids tendered, which was below the auction target of GHS 3.478 billion.

Auction Target | GHS 3.478 billion |

Total Bids | GHS 3.110 billion |

Total Accepted | GHS 3.110 billion |

Bid-to-Cover | 1.0000x |

Subscription Ratio | 0.8944x |

Money Market Term(s) of the Week

SOFR: SOFR stands for the Secured Overnight Financing Rate. It’s a key interest rate benchmark that serves as an alternative to LIBOR (London Interbank Offered Rate) in the United States. SOFR reflects the cost of borrowing cash overnight collateralized by Treasury securities. SOFR was developed by the Federal Reserve and the Federal Reserve Bank of New York as a replacement for LIBOR, which has been subject to manipulation and lacks sufficient transaction data.

{kind=link}