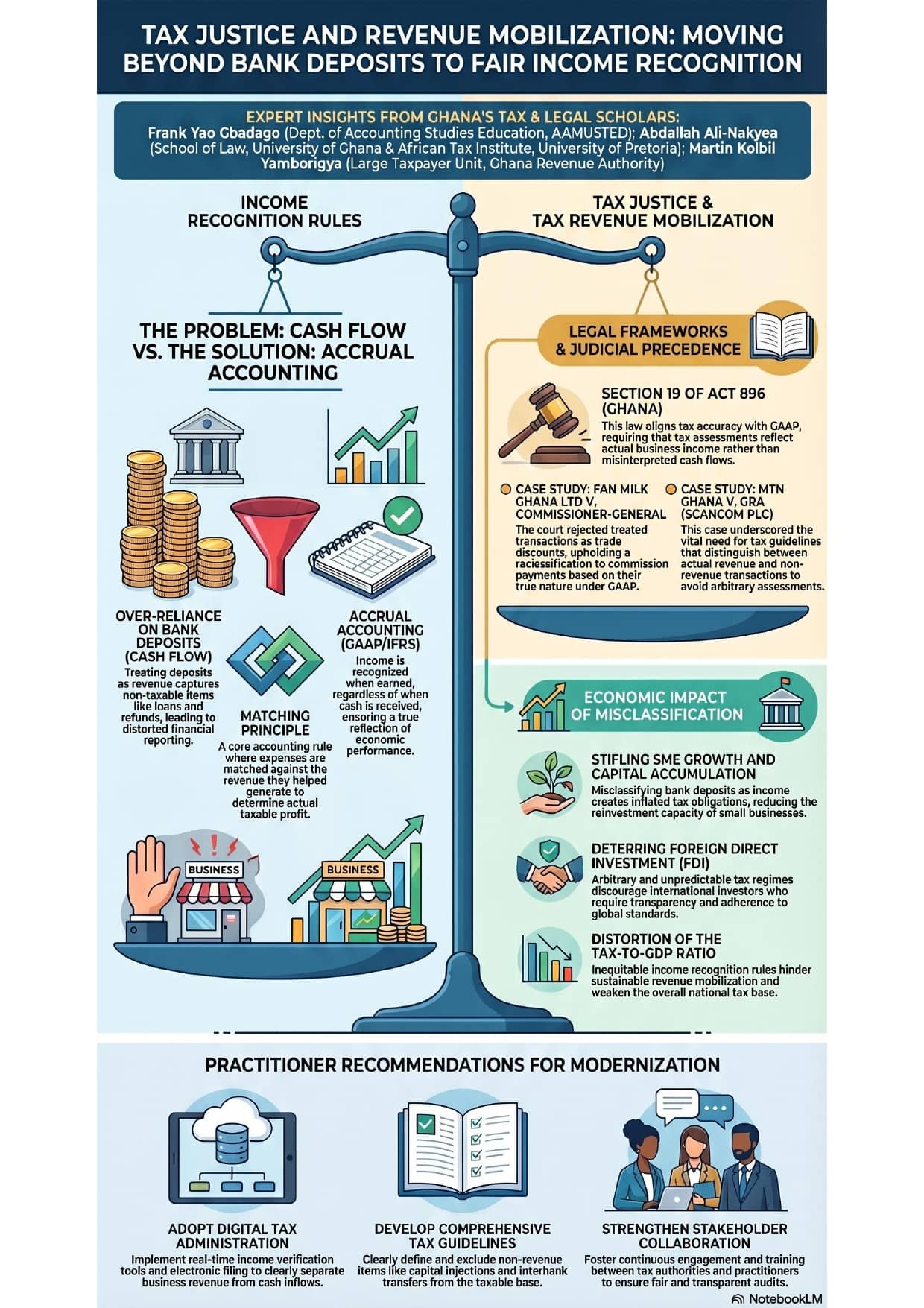

Tax policy experts have called for a fundamental shift in Ghana’s income recognition framework, urging policymakers to move away from the over-reliance on bank deposits as a basis for taxation.

The experts observed that the adoption of accrual-based accounting principles would improve fairness for both tax authorities and taxpayers while enhancing revenue mobilisation.

The call was made in a policy-focused analysis that featured insights from tax and legal scholars, including Dr. Dr. Frank Yao Gbadago of the Department of Accounting Studies Education at AAMUSTED, Abdallah Ali-Nakyea of the University of Ghana School of Law and the African Tax Institute at the University of Pretoria, and Dr. Martin Kolbil Yamborigya, Commissioner of the Domestic Tax Revenue Division (DTRD) of the Ghana Revenue Authority (GRA).

At the centre of the argument was the concern that treating bank deposits as taxable income distorted true business performance by capturing non-taxable inflows such as loans, capital injections, and refunds.

According to the experts, this practice could inflate taxable income and result in unfair assessments, particularly for small and medium-sized enterprises.

They argued that a shift towards accrual accounting—aligned with global standards such as GAAP and IFRS—would ensure income was recognised when it was earned, rather than when cash was received.

This, they noted, provided a more accurate reflection of a business’s economic activity and supported the “matching principle,” where expenses were aligned with the revenues they generated.

The discussion also highlighted legal backing for improved income recognition. Section 19 of Ghana’s Income Tax Act, 2015 (Act 896), was cited as aligning tax assessments with actual business income rather than misinterpreted cash flows, reinforcing the need for substance over form in tax administration.

Judicial precedents further supported this position. The analysis referenced landmark tax disputes such as the case involving MTN Ghana Limited and the Commissioner-General, where the courts emphasised the importance of correctly classifying transactions based on their true economic nature under accounting standards.

It also pointed to rulings involving Fan Milk and a case involving Scancom PLC and the Ghana Revenue Authority, which underscored the need to distinguish revenue from non-revenue inflows to prevent arbitrary tax assessments.

Beyond legal interpretation, the experts warned that misclassification of income had wider economic implications.

They argued that inflated tax liabilities could stifle SME growth by reducing reinvestment capacity, while also discouraging foreign direct investment due to perceived unpredictability in tax administration. Over time, such distortions could also weaken the tax-to-GDP ratio by eroding trust and efficiency in the tax system.

To address these challenges, the analysis recommended modernisation of tax administration through digital tools that enabled real-time income verification and clearer separation of revenue from non-revenue inflows.

It also called for the development of comprehensive tax guidelines to explicitly exclude items such as capital injections and interbank transfers from taxable income calculations.

Strengthening collaboration between tax authorities, practitioners, and businesses was also highlighted as essential to improving compliance, audit fairness, and overall transparency in the tax system.

The experts maintained that aligning Ghana’s tax system with accrual-based income recognition principles was critical not only for fairness in taxation but also for sustainable revenue mobilisation and long-term economic stability.

{kind=link}