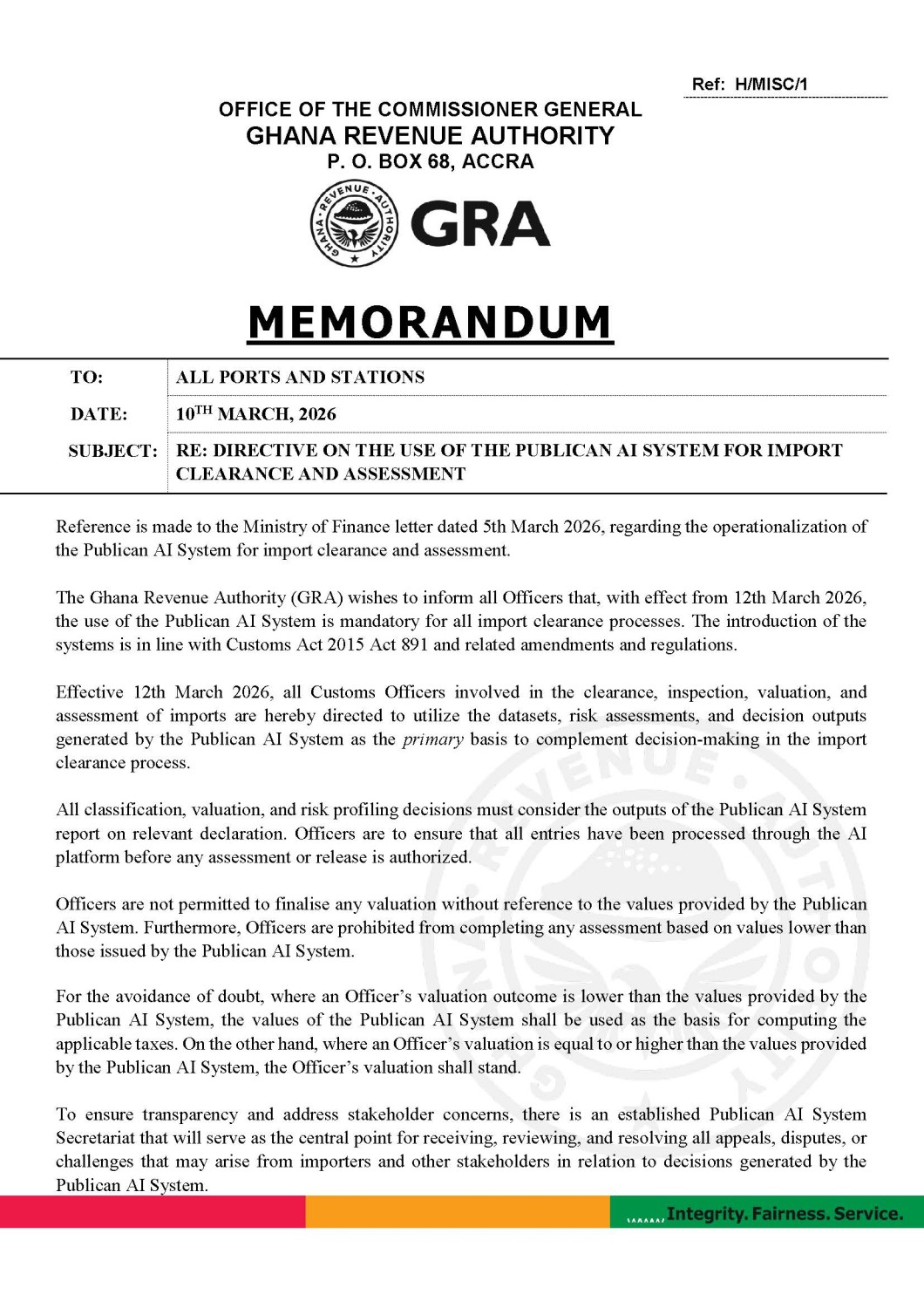

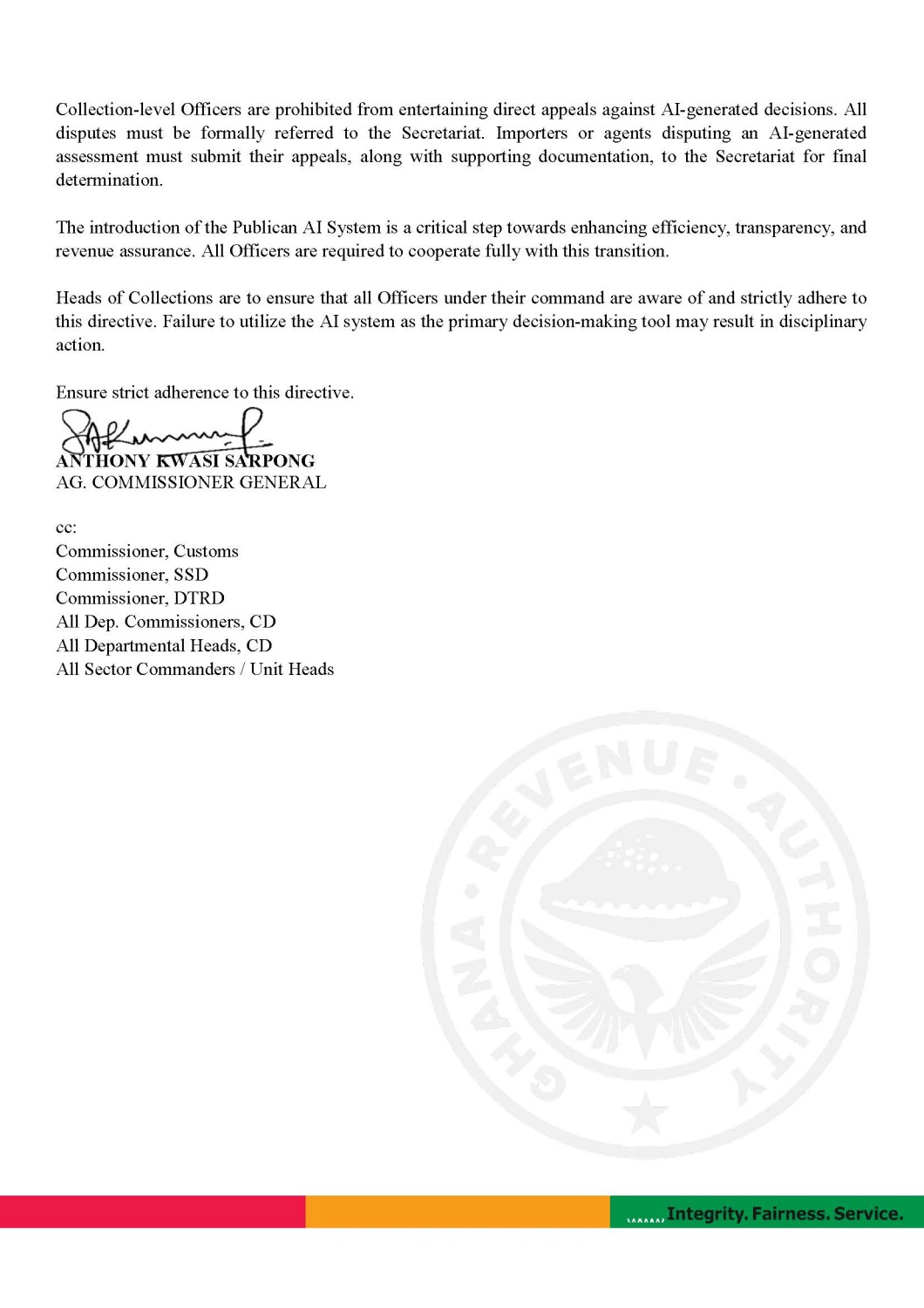

Ghana’s customs administration has entered a decisive new phase. The GRA has issued a directive mandating the use of an AI-driven system for import valuation known as the Publican AI System. This AI-powered system is the primary basis for import valuation and clearance. At a policy level, this move is both timely and understandable, and the objective is unmistakable: to strengthen revenue mobilisation, reduce discretion, and modernise border processes through data-driven tools. However, this new policy has clearly struck a nerve across the trade ecosystem. For years, customs administrations in Ghana have grappled with under-invoicing, valuation disputes, and inconsistent treatment of import declarations. In this context, deploying AI to generate datasets, risk profiles, and valuation benchmarks represents a deliberate shift toward automation, standardisation, and control. It is, in many respects, the natural evolution of customs administration.

Yet, recent reactions from freight forwarders, traders, and industry groups point to a growing unease, including concerns about overvaluation, lack of transparency, and reduced human discretion. At the same time, the Ministry of Finance has taken a firm stance, warning against any attempts to undermine what it sees as a critical reform tool. This tension is not surprising, but it is telling. It is a contest over how customs valuation should fundamentally work.

The policy rationale

The rationale behind the system is compelling. If customs administrations face challenges with under-invoicing, revenue leakages, and inconsistent valuation practices, then an AI system promises standardisation, predictability, and data-driven valuation. This certainly replaces negotiated valuation, and for the GRA, that is not just reform—it is control.

The stakeholder pushback

Across the trade ecosystem, concerns are emerging with increasing intensity, and these concerns cannot be dismissed lightly. There are allegations of inflated valuation benchmarks, complaints about reduced transparency, and anxiety over the erosion of professional discretion. Specifically, freight forwarders are questioning the fairness of imposed values, traders are highlighting the financial burden of inflated assessments, and agents are calling for review and recalibration of the system. At the same time, the policy direction from government remains firm. The Publican AI system is a necessary intervention to curb abuse and safeguard revenue. This tension is not unusual; it is, in fact, the hallmark of any major structural reform. But beneath the surface lies a more fundamental question: is the system merely supporting valuation, or is it redefining it?

The legal tension or policy risk: AI vs established valuation principles

The global standard governing customs valuation, established under the World Trade Organization Agreement on Customs Valuation (ACV), rests on a foundational rule. The primary rule is simple: customs value must be based on the transaction value (the actual price paid or payable for the goods). Any departure from this rule is an exception, not the norm. This principle is not just procedural; it is the bedrock of fairness in international trade.

Transaction value is not automatic. Customs may reject it, but only under specific, justifiable conditions such as related-party transactions and influence (where the buyer and seller are related and the relationship affects the price), doubts about transaction value accuracy (where there are reasonable grounds to believe the declared value is false, e.g., under-invoicing or fraud), or lack of documentation by the importer. Even in these circumstances, customs must provide reasons and give the importer an opportunity to justify the value. If transaction value is rejected, the rules require authorities to follow a strict sequence, not discretion:

a. Transaction Value of Identical Goods (use the value of exactly the same goods imported at or about the same time).

b. Transaction Value of Similar Goods (use the value of comparable goods with similar characteristics and function).

c. Deductive Value Method (based on the resale price in the importing country, less costs such as profit, transport, and duties).

d. Computed Value Method (based on cost of production plus profit and expenses in the country of export).

e. Fallback Method (a flexible method using reasonable means consistent with WTO principles, but not arbitrary or based on minimum values).

These methods must be applied in order unless the importer requests a switch between the deductive and computed value methods.

Ghana’s shift from transaction value to AI benchmarks

The directive by the GRA introduces a mandatory AI-driven valuation system (Publican) as the central basis for customs assessments. Under the Publican system, all import declarations must be processed through the system, and its outputs serve as the default benchmark for determining customs value. In practice, the directive restricts customs officers from accepting declared values below AI-generated outputs and effectively establishes the AI value as a minimum valuation threshold. Any deviation from the system’s values must undergo centralised review and approval.

This is where the legal concern crystallises. The directive, by prohibiting customs officers from finalising valuations below AI-generated outputs and requiring those outputs to prevail where lower values appear, is in substance operating as a de facto minimum valuation regime under the banner of artificial intelligence. Under WTO rules, the use of minimum or reference values as binding benchmarks is expressly discouraged. Recall the benchmark regime introduced by the government in 2022, applied to the home delivery value of imports, originally set at 50% for general goods and 30% for vehicles to boost port competitiveness. It was implemented as a “discount” regime to avoid creating legal tension in global trade.

Generally, customs authorities are empowered to question declared values, but only within a structured, sequential framework and with proper justification. What they cannot do is replace the transaction value with a predetermined or system-generated figure as a default. This raises a difficult but necessary question: are we using AI to validate transaction values, or to replace them? If the system effectively sets a minimum benchmark, it begins to resemble a reference pricing regime, which sits uneasily within WTO valuation principles. This is not just a technical issue; it is a structural one.

A deeper policy shift?

What we are witnessing is not just a technological upgrade; it is a philosophical shift—from human-led discretion to system-led determination. On one hand, this AI-driven system reduces manipulation, inconsistency, and discretionary abuse in the assessment of customs duties. On the other hand, it introduces rigidity in complex transactions, over-reliance on algorithmic outputs, and a system where the importer must now prove that the machine is wrong. In effect, the centre of gravity is shifting—from the officer to the algorithm.

What do we do then? Finding the balance

There is no doubt that technology will define the future of tax and customs administration. The answer is not to abandon the system—that would be a step backward. Ghana has taken a bold and necessary step toward digitising its customs administration. The introduction of AI is not the problem; indeed, it is part of the solution. The challenge lies in ensuring that innovation does not outpace the law. Ghana can benefit if the AI system serves as a risk and validation tool, not a binding valuation authority that replaces the judgment of customs officers. Again, transaction value should remain the legal foundation, but officers must be given reasoned discretion. Finally, importers must be given credible and transparent avenues for challenge. The goal is not to replace the law with technology, but to ensure that technology operates within the law.

Final thought

Every major reform generates resistance, but resistance, when properly understood, is not always opposition; it is often feedback. Ghana has taken a bold step toward modernising customs administration. The real test, however, is not whether the system works, but whether it works within the law. Transaction value remains the legal foundation of customs valuation. AI outputs should be treated as indicative, not binding, and officers must retain some discretion grounded in evidence.

Francis Timore Boi is a Ghanaian lawyer and policy analyst specialising in taxation, customs administration, and public financial management. He provides thought leadership on fiscal policy and regulatory reforms in Ghana.

DISCLAIMER: The views, comments, and contributions made by readers or contributors on this website do not necessarily represent the position or views of The Sikaman Times. The Sikaman Times will not be responsible or liable for any inaccurate or incorrect statements made by readers or contributors on this website.

{kind=link}